Calculating Exchange Rate Risk and Volatility in Historical Trade

International trade has always been a dance with uncertainty, from unpredictable weather to shifting political landscapes. Yet, one of the most persistent challenges is the fluctuation of currency values. Understanding historical exchange rate risk is crucial because it reveals the financial tightrope that businesses walk when their costs and revenues are in different currencies, where a sudden shift can turn a profitable venture into a significant loss.

At its core, exchange rate risk—often called FX risk—is the possibility of financial loss stemming directly from changes in currency exchange rates. This risk became a central concern for global businesses after the world moved away from fixed currency systems, forcing companies to develop sophisticated methods for calculating and managing the inherent volatility in foreign exchange markets. This article explores how this risk evolved, the tools used to measure it, and the strategies developed to navigate it.

The Historical Context: A World Before and After Bretton Woods

For much of the mid-20th century, international business was relatively sheltered from currency volatility. The Bretton Woods Agreement, established after World War II, created a system of fixed exchange rates. Most major currencies were pegged to the U.S. dollar, which was, in turn, convertible to gold at a fixed price.

During this period, businesses faced minimal exchange rate risk. A deal made in German Deutsche Marks or British Pounds had a predictable value in U.S. dollars, simplifying international accounting and trade finance. This stability, however, was not destined to last.

In 1973, the Bretton Woods system collapsed, leading to the adoption of floating exchange rates. Currencies were no longer pegged and began to “float,” with their values determined by market forces of supply and demand. This seismic shift introduced a new era of volatility and exposed firms to significant financial risks they had never needed to manage before.

The Three Faces of Exchange Rate Risk

As businesses grappled with this new reality, experts began categorizing exchange rate risk into three distinct types. Each type affects a company’s finances differently, from immediate cash flow to long-term strategic value.

1. Transaction Risk

Transaction risk is the most direct form of exchange rate risk. It arises from the time delay between entering into a contract and settling it. For example, a U.S. company might agree to sell goods to a customer in Japan for ¥10 million, with payment due in 90 days.

- If the yen weakens against the dollar during that 90-day period, the ¥10 million will convert to fewer dollars, eroding the U.S. company’s profit.

- Conversely, if the yen strengthens, the company will receive more dollars than anticipated, resulting in a windfall gain.

This uncertainty directly impacts the profitability of individual international deals, making it a primary focus for corporate treasurers.

2. Translation (Accounting) Risk

Translation risk, also known as accounting risk, is related to a company’s financial reporting. Multinational corporations must consolidate the financial statements of their foreign subsidiaries into their home currency for reporting purposes. When exchange rates fluctuate, the reported value of foreign assets and liabilities changes.

For instance, a French parent company with a subsidiary in the United Kingdom will see the euro-denominated value of its UK assets shrink if the pound sterling depreciates. While this may not involve an immediate cash loss, it can negatively impact reported earnings and a company’s balance sheet, influencing investor perceptions and stock prices.

3. Economic (Operating) Risk

Economic risk is the most complex and long-term form of exposure. It refers to the impact of unexpected, persistent exchange rate movements on a company’s future cash flows and overall market competitiveness. This risk is not just about specific transactions but about the fundamental value of the business.

Consider a German automaker that competes with American manufacturers. If the euro strengthens significantly against the U.S. dollar over several years, the German cars become more expensive for American buyers. This could lead to a loss of market share and reduced long-term profitability, even if the company isn’t directly involved in U.S. dollar transactions.

Measuring Volatility in Currency History

The history of floating exchange rates is punctuated by periods of extreme volatility, often driven by geopolitical turmoil and economic crises. These events serve as stark reminders of the destructive potential of unmanaged currency risk. Major historical currency crises, such as those in Mexico (1994), Southeast Asia (1997), Russia (1998), and Argentina (early 2000s), saw currencies devalue dramatically in short periods.

During the 1997 Asian Financial Crisis, for example, some currencies depreciated by over 50% in just a few months. Such events caused widespread corporate bankruptcies and demonstrated that exchange rate risk could threaten entire economies. To protect against such outcomes, financial experts developed statistical methods to measure and predict this volatility.

Key Statistical Tools for Risk Calculation

Calculating exchange rate risk requires a quantitative approach. Over the years, risk managers have come to rely on several key statistical models:

- Standard Deviation: This is a fundamental statistical measure of dispersion or volatility. A higher standard deviation for a currency pair’s exchange rate indicates greater historical volatility and, therefore, higher risk.

- Value at Risk (VaR): VaR is a more sophisticated model that estimates the potential financial loss over a specific time horizon for a given confidence level. For example, a VaR calculation might conclude that a company has a 5% chance of losing at least $10 million over the next month due to FX movements. Banking regulators, often following guidelines from bodies like the Bank for International Settlements (BIS), require firms to use models like VaR to quantify and report their risk exposures.

The Rise of the Historical FX Volatility Index

While traders have always measured daily price movements, the creation of standardized indices provided a more accessible way to gauge market sentiment. A historical FX volatility index, such as the JPMorgan G7 FX Volatility Index or Deutsche Bank’s CVIX, consolidates the volatility of major currency pairs into a single, easy-to-track number.

These indices are relatively recent innovations, but they build on long-standing practices. Financial professionals have long used a currency pair’s “implied volatility”—derived from the pricing of currency options—to summarize the market’s expectation of future fluctuations. This forward-looking measure is invaluable for setting hedging strategies and pricing financial instruments.

The Evolution of Hedging History

The move to floating rates in the 1970s was the catalyst for the modern era of financial hedging. Companies could no longer afford to leave their currency exposures unmanaged. This necessity sparked innovation in financial markets, leading to the development of derivatives designed specifically to mitigate exchange rate risk.

This marks the beginning of modern hedging history, where proactive risk management became a core function of corporate finance. The primary tools developed during this time remain pillars of risk management today.

Primary Hedging Instruments

- Forward Contracts: A forward contract is a simple yet powerful tool. It is a binding agreement to exchange a specific amount of one currency for another at a predetermined exchange rate on a future date. This effectively locks in the exchange rate, eliminating transaction risk entirely for a specific deal.

- Currency Options: An option provides more flexibility. It gives the holder the right, but not the obligation, to exchange currency at a set rate by a specific date. This allows a company to protect itself from unfavorable rate movements while still benefiting from favorable ones, in exchange for paying a premium for the option.

Other tools, such as futures contracts, swaps, and balance-sheet hedging (offsetting foreign currency assets with liabilities in the same currency), also became common practice.

Modern Techniques for Managing Currency Risk in Trade

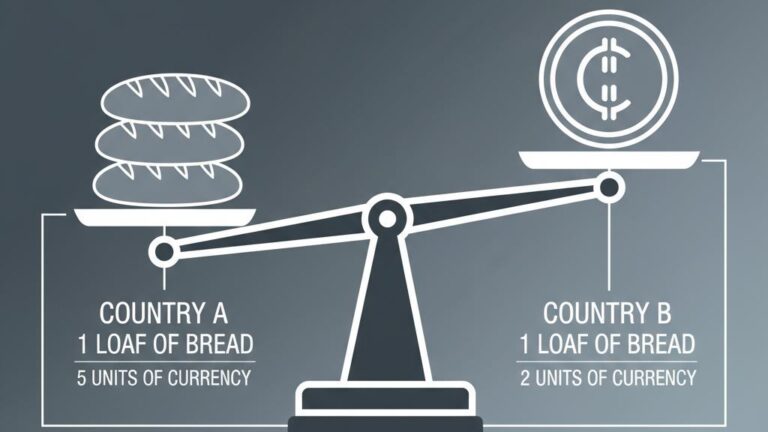

Today, managing currency risk in trade is a highly sophisticated discipline that blends strategy, statistics, and technology. Modern businesses employ a comprehensive framework to identify, measure, and mitigate their FX exposures. For anyone interested in the specifics of currency values, tracking values through history provides essential context.

The modern approach typically involves several key steps:

- Risk Identification and Measurement: Companies conduct detailed analyses of their operations to identify all sources of transaction, translation, and economic risk. They use scenario analysis and statistical modeling, such as VaR, to quantify these exposures. The International Monetary Fund offers extensive research on these approaches for firms.

- Policy Formation: Corporate treasury departments establish formal hedging policies. These policies outline the company’s risk tolerance and set clear procedures and limits for using financial derivatives.

- Derivative Usage: Businesses actively use forwards, options, and swaps to hedge their identified risks, locking in rates to protect profit margins and reduce earnings volatility.

- Natural Hedging: Whenever possible, companies structure their operations to create natural offsets. For example, a company might build a factory in a country where it has significant sales, ensuring that both its costs (labor, materials) and revenues are in the same currency.

- Technology and Automation: Modern treasury management systems and real-time FX analytics platforms allow for continuous monitoring of currency exposures. These tools enable finance teams to react quickly to market changes and implement hedging strategies efficiently.

Frequently Asked Questions

What is historical exchange rate risk?

Historical exchange rate risk refers to the potential for financial loss due to changes in foreign currency values over time. This risk affects the value of international transactions, assets, and investments when they are denominated in a currency other than a company’s home currency.

How has exchange rate risk changed since the collapse of the Bretton Woods system?

The collapse of the Bretton Woods system in 1973 marked a shift from fixed to floating exchange rates. This change dramatically increased currency volatility, forcing businesses to actively manage and hedge their currency exposures for the first time in the modern era.

What are the main ways companies hedge against exchange rate risk?

Companies commonly use financial instruments like forward contracts, currency options, and swaps to lock in future exchange rates. They also employ strategies like natural hedging, which involves matching costs and revenues in the same foreign currency.

How do financial professionals measure exchange rate volatility?

Volatility is typically measured using statistical tools like standard deviation, which gauges historical price dispersion, and Value at Risk (VaR), which estimates potential losses. Professionals also use specialized FX volatility indices to track market-wide risk sentiment.

Conclusion

The journey from the stable world of Bretton Woods to the dynamic environment of floating currencies has fundamentally reshaped international business. Calculating and managing historical exchange rate risk has evolved from a niche concern into an essential component of corporate strategy. By understanding the different types of risk, using statistical tools to measure volatility, and employing sophisticated hedging strategies, businesses can navigate the complexities of global markets.

Ultimately, a proactive and well-defined approach to currency risk management is not just about preventing losses; it is about creating financial stability and protecting a company’s long-term competitive advantage. To gain a deeper understanding of how currency values are determined and tracked over time, exploring resources on historical exchange rates can provide valuable insight.