The Predecessors of the Euro: ECU, EMS, and European Integration

The euro is one of the world’s most significant currencies, but its existence is the result of a long and complex journey toward European monetary union. It didn’t emerge from a vacuum; it was built upon decades of experiments, frameworks, and foundational concepts. Understanding the predecessors of the euro is key to appreciating the single currency’s historical and economic significance.

The most important of these forerunners were the European Monetary System (EMS) and its innovative accounting tool, the European Currency Unit (ECU). These systems provided the technical and political runway for the eventual creation of the euro, serving as a critical bridge from a continent of disparate national currencies to a unified monetary bloc.

The Historical Drive for European Monetary Integration

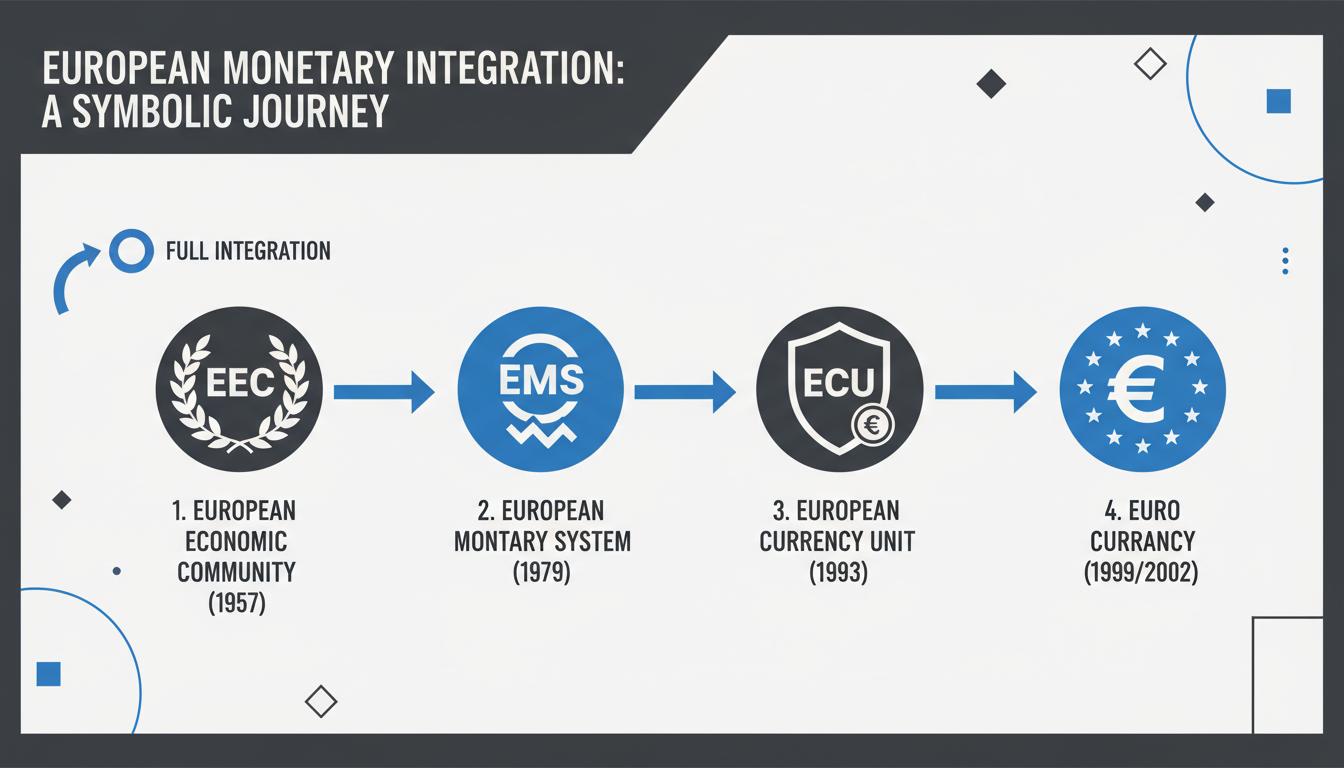

The ambition for a unified European currency has roots in the post-World War II desire for lasting peace and economic stability. Early milestones like the Treaty of Rome in 1957, which established the European Economic Community (EEC), set the stage for deeper cooperation. However, the need for monetary stability became urgent in the 1970s.

The collapse of the Bretton Woods system, which had pegged global currencies to the U.S. dollar, unleashed a period of intense exchange rate volatility. European nations, with their highly interconnected economies, found this instability damaging to trade and economic planning. This chaos gave rise to the 1970 Werner Report, an early blueprint for achieving economic and monetary union over the following decade.

The European Monetary System (EMS): A Framework for Stability

In response to the currency turmoil, the European Monetary System (EMS) was launched in 1979. Its primary goal was to create a zone of monetary stability in Europe, reduce exchange rate fluctuations, and foster closer economic policies among EEC member states. The system was a major step in the history of European integration currency policy.

The core of the EMS was the Exchange Rate Mechanism (ERM). This mechanism established a system of fixed but adjustable exchange rates, where each participating currency was given a central rate against the others. Currencies were allowed to fluctuate within narrow bands around these central rates.

How the ERM Worked

If a currency’s value approached the upper or lower limit of its band, the central banks of the involved countries were obligated to intervene. They would buy or sell the currency on open markets to bring its value back within the agreed-upon limits. This created a system of mutual support and collective responsibility for exchange rate stability.

However, participation was not universal. The United Kingdom, for example, initially chose not to join the ERM, highlighting the political challenges and varying levels of commitment to monetary integration among member states.

The European Currency Unit (ECU): The Euro’s Direct Predecessor

While the EMS provided the framework, its most significant innovation was the European Currency Unit (ECU). The ECU was the central pillar of the EMS, serving as the official unit of account for the EEC. The European Currency Unit ECU history is fascinating because it was a currency that existed more in theory and on balance sheets than in people’s pockets.

What Was the ECU?

The ECU was a composite, or “basket,” currency. Its value was derived from a weighted average of the currencies of the participating EEC members. It was an artificial currency—no physical ECU banknotes or coins were ever minted for public circulation.

Instead, its primary functions were:

- A unit of account: Used for EEC budgets and transactions between community institutions.

- A financial instrument: Widely used in private financial markets for issuing bonds and denominating contracts.

- A reserve asset: Held by central banks as part of their foreign exchange reserves.

Composition of the ECU Basket

The ECU’s value was determined by the combined value of its constituent currencies. The basket included fixed amounts of each currency, with the weighting of each reflecting the economic size of its respective country. The currencies in the basket included:

- German Mark

- French Franc

- Italian Lira

- Dutch Guilder

- Belgian Franc

- Danish Krone

- Irish Pound

- Greek Drachma

- Spanish Peseta

- Portuguese Escudo

- Luxembourg Franc

The composition of this basket was not static. It was periodically adjusted to account for shifts in economic weight and the accession of new member states to the EEC.

The ECU’s Surprising Influence in Global Finance

Though it never became a public currency, the ECU achieved remarkable success in international capital markets. Because its value was based on a basket of currencies, it was more stable than any single national currency. This stability made it highly attractive to international investors and borrowers.

By the early 1990s, the ECU had become the second-most widely used currency for international bond issues, trailing only the U.S. dollar. This success helped familiarize global markets with the concept of a pan-European currency, paving the way for the institutional framework established by the Maastricht Treaty in 1992.

Early Predecessors of the Euro: Lessons from History

The idea of a European monetary union was not entirely new. History provided important, if cautionary, examples of earlier attempts at currency integration. These historical precedents offered valuable lessons for the architects of the euro.

Two notable examples include:

- The Latin Monetary Union (1865–1927): Led by France, this union aimed to standardize the weight and composition of gold and silver coins across several European countries.

- The Scandinavian Monetary Union (1873–1914): This union established a common gold standard and interchangeable currencies among Denmark, Norway, and Sweden.

Both unions ultimately failed, largely because they lacked the necessary political and fiscal integration to withstand major economic shocks and diverging national policies. As noted in research from the National Bureau of Economic Research (NBER), these early unions demonstrated that monetary cooperation without deeper institutional unity is fragile. This lesson was central to the design of the Eurozone, which included creating institutions like the European Central Bank (ECB).

The Transition: From ECU and Pre-Euro Currency to the Euro

The experience with the EMS and ECU was invaluable, but it also revealed weaknesses. The currency crises of 1992–1993, when speculative attacks forced several countries out of the ERM, demonstrated that fixed-but-adjustable exchange rates were vulnerable without a full monetary union.

This realization provided the final impetus for the creation of a single currency. On January 1, 1999, the euro was introduced as an electronic currency for banking and financial transactions. The transition from the ECU was remarkably smooth, as the euro replaced the ECU at a 1:1 parity. All existing ECU-denominated contracts and bonds were automatically converted into euros.

For the next three years, legacy national currencies—the various forms of pre-euro currency like the Deutsche Mark, French franc, and Spanish peseta—continued to circulate as subdivisions of the euro. Finally, on January 1, 2002, euro banknotes and coins were introduced, and the old national currencies were gradually withdrawn from circulation.

Conclusion: The Legacy of the Euro’s Predecessors

The journey to the euro was a gradual process of evolution, marked by both successes and failures. The European Monetary System provided a crucial training ground for monetary cooperation, while the European Currency Unit served as a practical and symbolic bridge to a single currency. By familiarizing markets with a stable, pan-European unit of account, the ECU made the final leap to the euro technically and politically achievable.

These predecessors were not mere historical footnotes; they were essential components in one of the most ambitious monetary projects in history. This entire journey laid the groundwork for the modern currency, a story detailed in the creation of the euro.

Frequently Asked Questions

What was the European Currency Unit (ECU)?

The ECU was a notional basket currency composed of fixed amounts of EEC member currencies. It was used as a unit of account and financial instrument within the European Monetary System from 1979 to 1999, after which it was replaced by the euro at a 1:1 rate. For more details, Britannica offers a comprehensive overview.

How did the European Monetary System (EMS) work?

The EMS was a framework that set currency fluctuation bands (via the Exchange Rate Mechanism) among participating countries. It relied on mutual central bank interventions to maintain stability and used the ECU as a common reference. The Centre Virtuel de la Connaissance sur l’Europe provides detailed historical documents on the EMS.

What role did the ECU play in the transition to the euro?

The ECU provided a stable, supranational unit of account that familiarized markets with a pan-European currency. It facilitated financial integration and served as the direct technical predecessor to the euro, which replaced it at a one-to-one value.

Were there predecessors to the idea of European monetary union before the ECU?

Yes, previous examples include the Latin Monetary Union and Scandinavian Monetary Union in the 19th and early 20th centuries. These unions tried but ultimately failed to sustain regional monetary integration, providing valuable lessons about the need for deeper political and fiscal union.

Which currencies composed the ECU basket?

The ECU’s basket included the German mark, French franc, Italian lira, Dutch guilder, Belgian franc, Danish krone, Irish pound, Greek drachma, Spanish peseta, Portuguese escudo, and Luxembourg franc. The weights of each currency in the basket were designed to reflect each country’s relative economic strength.