Historical Interest Rate Differentials and Currency Flow

Global finance is a vast ocean of capital, constantly shifting from one shore to another. While headlines often focus on stock market rallies or geopolitical tensions, one of the most powerful undercurrents is the gap between national interest rates. A deep dive into historical interest rate differentials reveals a compelling story of how these seemingly small percentages have directed massive currency flows, shaped investment strategies, and defined entire economic eras.

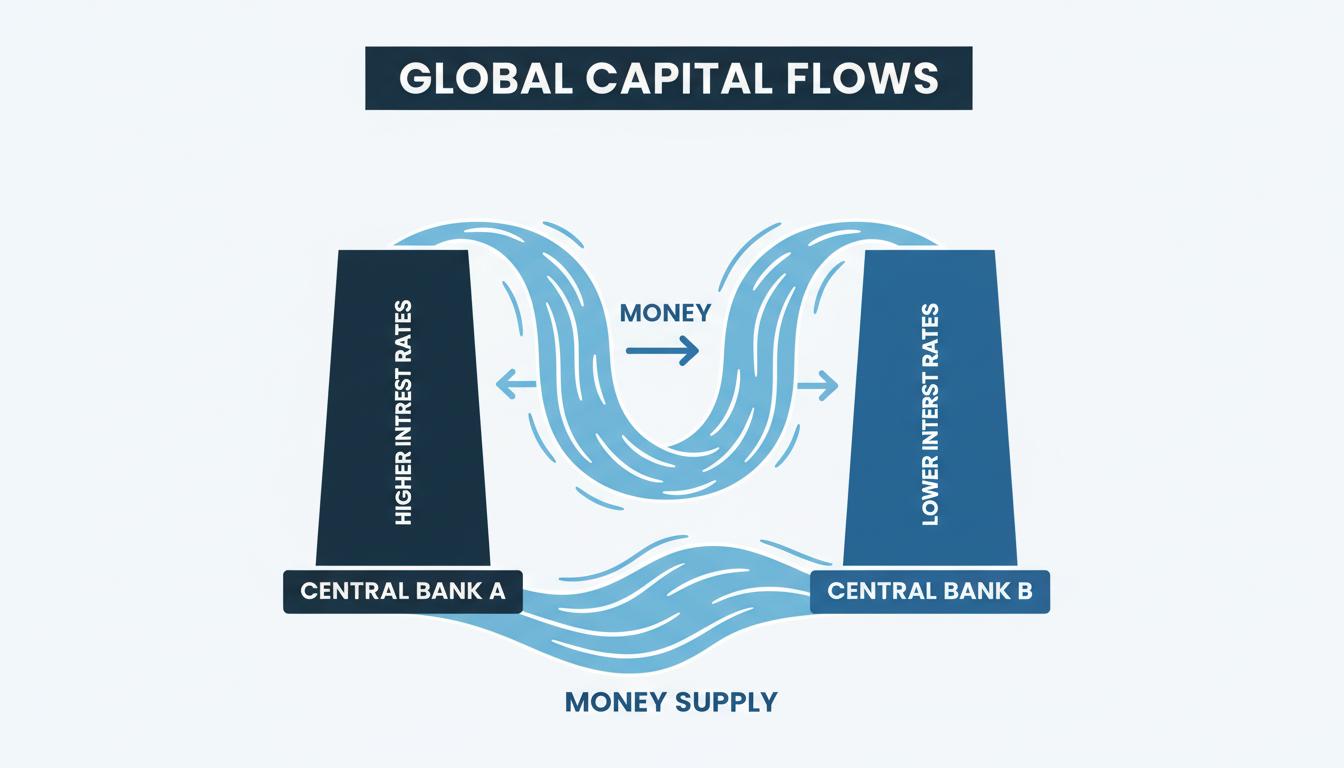

An interest rate differential (IRD) is simply the difference between the benchmark interest rates of two countries. This single number acts as a powerful magnet for global capital, influencing everything from the value of a currency to the stability of a nation’s debt. By understanding how these differentials have evolved, we can better grasp the history of global capital flows and the forces that continue to shape our interconnected economy.

What Are Interest Rate Differentials? The Core Concept

At its heart, an interest rate differential is a straightforward calculation. It quantifies the gap between the policy rates or bond yields of two different economies.

The basic formula is:

IRD = i_domestic – i_foreign

Here, ‘i’ represents the relevant interest rate for each country. For example, if the U.S. Federal Reserve sets its federal funds rate at 3% and the Bank of Japan maintains its rate at 0.5%, the interest rate differential is 2.5%. This gap represents the extra return an investor could theoretically earn by holding assets in the higher-yielding currency, assuming the exchange rate remains stable.

The Theory of Interest Rate Parity

Economic theory provides a framework for understanding IRDs called Interest Rate Parity (IRP). This principle suggests that the differential between two countries’ interest rates should be perfectly offset by the expected change in their exchange rate. In a perfect market, this would eliminate any risk-free profit (arbitrage) from simply moving money between currencies to capture the higher yield. However, in the real world, this parity doesn’t always hold, creating opportunities and risks that have driven historical exchange rates for decades.

A Brief History of Global Capital Flows and Interest Rates

The connection between interest rates and currency values is not a new discovery. The famed British economist John Maynard Keynes highlighted its significance as early as 1923. However, the concept took center stage in the 1970s and 1980s.

During this period, several key shifts occurred:

- Market Liberalization: Many developed economies relaxed capital controls, allowing money to flow more freely across borders.

- Globalization: Financial markets became increasingly interconnected, creating a single global pool of capital.

- Volatile Exchange Rates: The collapse of the Bretton Woods system in 1971 led to more volatile exchange rates as countries adopted floating exchange rate regimes, making currency movements a critical factor in investment returns.

These developments amplified the importance of IRDs, turning them into a primary driver of international investment behavior. For instance, major rate hikes in the U.S. during the 1980s created large differentials that attracted significant capital, strengthening the U.S. dollar.

How Interest Rates and Exchange Rates History are Linked

Empirical data consistently shows a strong link between interest rate differentials and currency movements. When a country offers a higher interest rate compared to another, it tends to attract capital from investors seeking better returns. This influx of demand for the country’s currency causes it to appreciate.

The Magnet Effect in Action

A classic example occurred in the late 1990s and early 2000s. During this time, U.S. money market yields were up to 3 percentage points higher than those in the euro area. This substantial gap fueled massive demand for U.S. dollar-denominated assets, contributing to the dollar’s strength. These capital flows don’t just affect currency markets; they spill over into bond markets, stock exchanges, and even foreign direct investment, fundamentally altering the financial landscape.

It’s crucial to note that exchange rate movements are often amplified by investor expectations. The actual change in a currency’s value can exceed the interest rate differential itself, as traders and investors price in future central bank moves and overall economic sentiment.

High Interest Currency History and the Carry Trade

The persistent existence of IRDs gave rise to a popular investment strategy known as the “carry trade.” This strategy directly exploits the interest rate gap between two currencies.

What is the Carry Trade?

The carry trade involves borrowing money in a currency with a low interest rate (a “funding currency”) and investing it in a currency with a high interest rate (a “high-yielder”). Investors aim to profit from two sources:

- The Interest Differential: The direct profit from the gap between the borrowing and lending rates.

- Stable Exchange Rates: The strategy relies on the high-yielding currency remaining stable or appreciating against the funding currency.

This approach became a cornerstone of the carry trade and interest rates nexus in global finance. Historically, currencies with persistently high interest rates, such as the Australian dollar (AUD), New Zealand dollar (NZD), and the Turkish lira (TRY), became popular targets for carry traders.

The Inherent Risks

While potentially profitable, the carry trade is notoriously risky. The strategy can become crowded, and a sudden shift in market sentiment can trigger a rapid unwind. During periods of global stress or “risk-off” episodes, investors rush to exit these trades, causing the high-yielding currency to depreciate sharply. This can wipe out all gains from the interest differential and lead to significant losses, sometimes contributing to wider historical currency crises.

Major Trends in Historical Interest Rate Differentials

The landscape of interest rate differentials has undergone dramatic shifts, particularly in the 21st century.

The Post-2008 Financial Crisis Era

Following the 2008 Global Financial Crisis, IRDs between advanced economies narrowed dramatically. Central banks across the world, including the U.S. Federal Reserve and the European Central Bank, slashed interest rates to near-zero and implemented unconventional policies like quantitative easing. This synchronized policy response compressed the differentials that had previously driven large capital flows.

Sovereign Debt and the ‘r-g’ Differential

During the European debt crisis, another type of differential gained prominence: the “r-g” differential. This measures the gap between the interest rate on government debt (r) and the country’s economic growth rate (g). A persistently positive r-g differential was seen as an indicator of unsustainable debt dynamics and heightened solvency risk for nations like Greece and Italy.

Recent Asymmetry (2015–2021)

The years following the initial crisis response were marked by persistently low or even negative IRDs. Research covering the G7 and Eurozone from 2000–2018 found an interesting asymmetry: positive IRDs (where one currency’s rates were higher) led to more significant currency appreciation than negative IRDs caused currency depreciation. This suggests the relationship is not always a simple mirror image.

Limitations: Why Differentials Aren’t Everything

While IRDs are a powerful force, they are not the sole driver of currency flows. Investors must consider a broader range of factors that can override the pure interest-rate incentive, especially during times of market stress. These include:

- Global Risk Appetite: In times of fear, investors often flock to “safe-haven” currencies like the U.S. dollar or Swiss franc, regardless of their interest rates.

- Central Bank Intervention: Direct actions by central banks to buy or sell their own currency can disrupt traditional relationships.

- Inflation and Political Factors: High inflation can erode real returns, while political instability can deter investment even in high-rate environments.

Frequently Asked Questions

What is an interest rate differential and why does it matter?

An interest rate differential (IRD) is the difference between two countries’ benchmark interest rates. It is crucial because it influences global capital flows, currency valuations, and cross-border investment decisions.

How do interest rate differentials affect exchange rates?

Typically, a higher interest rate in one country relative to another (a positive IRD) attracts investors seeking higher returns. This increased demand for the currency causes it to appreciate. However, the actual exchange rate movement can be amplified by other market forces like investor expectations.

What is the carry trade and how does it relate to IRDs?

The carry trade is an investment strategy that exploits IRDs. It involves borrowing in a currency with a low interest rate and investing in one with a higher rate, aiming to profit from both the interest spread and a stable or appreciating exchange rate.

Which currencies have historically had high interest rates?

Currencies like the Australian dollar (AUD), New Zealand dollar (NZD), and Turkish lira (TRY) have often offered higher interest rates than major economies. This has made them frequent targets for carry trade strategies, though they also carry higher risk.

Are interest rate differentials a reliable predictor of currency trends?

While IRDs are a key driver, they are not always reliable predictors on their own. Market expectations, central bank actions, geopolitical risks, and structural economic shifts can weaken or even override their effect on currency movements.

Conclusion

The history of global finance is inextricably linked to the ebb and flow of capital across borders, and interest rate differentials have long been the primary current guiding this movement. From the liberalization of the 1980s to the era of zero-interest rates after 2008, these gaps have created both immense opportunity and significant risk.

By studying historical interest rate differentials, we gain invaluable insight into the mechanics of the foreign exchange market and the complex interplay between monetary policy, investor psychology, and economic fundamentals. Understanding these past patterns is essential for navigating the ever-changing landscape of international finance.